1. Introduction

As the European Union (EU) evolves into a knowledge society, the competence to generate, use, diffuse and absorb new knowledge is increasingly viewed as critical for economic success and societal development. Against this background, conventional wisdom views so‐called high‐tech, research‐intensive and science‐based industries as the key drivers of future economic prosperity. Such industries are seen as the main source of highly sophisticated products that are not easily imitated elsewhere and, therefore, the policy conclusion is that high‐cost industrialised countries should concentrate their efforts on promoting these industries. In this scenario, low‐ and medium‐tech (LMT) industries are deemed to offer severely limited prospects for future growth in comparison to high tech ones, and as a result, receive less explicit policy attention and support. A critique of this widely held view is the starting point of an EU‐funded research project with the acronym PILOT—‘Policy and Innovation in Low‐Tech: Knowledge Formation, Employment and Growth Contributions of the “Old Economy” Industries in Europe’.1 This project was undertaken by a consortium of social scientists from 11 universities and research institutes in nine European countries.2

In the following sections, we outline the outcomes of PILOT and discuss the implications of our findings. Sections 2–4 investigate the activities and status of LMT industries, particularly within the EU, and review the adequacy of current innovation indicators. In Section 5, we present a brief overview of the successful innovation practices in LMT sectors in the absence of substantial investments in R&D as generally measured, while Section 6 considers the knowledge management and human resource bases of LMT firms, the role of embeddedness in local and regional economies in a period of increasingly important globalisation, and symbiotic relationships between LMT and high‐technology firms and sectors. Finally, Sections 7 and 8 look at some of the policy issues surrounding LMT sectors and at ways of improving their importance. Our overall conclusion is that the performance of LMT sectors is severely misrepresented by most current indicators and that they contribute very significantly to innovation and growth in advanced economies. LMT firms often face special problems, however, and their efficiency could be further improved through the implementation of appropriately targeted policies.

2. Challenges and Context of Research on Low‐tech Industries

The main starting point of research on low‐tech industries and of discussion on the development perspectives of such industries in the old industrialised countries of the European Union is a fundamental criticism of the widely held focus on high technology and necessitates a re‐examination of the relevance of LMT sectors. To a large extent, this one‐sided attention reflects the idea that ongoing societal change in modern societies can be characterised as typical of an emerging ‘Knowledge Society’3 or ‘Learning Economy’.4 These writers and others share the idea that modern organisations and societies are undergoing a fundamental change process, based on the enhanced significance of knowledge as a productive force and asset. Continual innovation, accompanied by a restructuring of work processes and organisation, is a decisive determinant of economic and social development, while the generation, diffusion and utilisation of knowledge is a core characteristic of firms and of economic activity as a whole.

To be sure, these discourses on the emerging knowledge society do describe important tendencies in economic and social development. We share the view that knowledge is an increasingly important resource, but we dispute much of the conventional wisdom about how the knowledge economy is structured and the implications for economic trends and hence policy measures. The knowledge economy is usually identified with a very small number of research‐based or science‐based activities, especially information and communications technologies (ICT) and biotechnology. Furthermore, it is often argued that as a consequence of increased knowledge intensity, the economies of industrialised countries in Europe and elsewhere are currently going through at least two great changes.5

- •

A significant part of industrial production is relocating from its traditional sites to developing countries. The classic example is the exodus of textiles from the rich world over the past three decades. This applies particularly to labour‐intensive ‘mature’ industries: quite soon, it is claimed, many big Western firms in such industries will have more employees and even customers in developing countries than in developed ones.

- •

In many industrialised countries the balance of economic activity is swinging from manufacturing to services. Even in Germany and Japan, which rebuilt so many factories after 1945, manufacturing’s general share of jobs in relation to the whole economy is declining rapidly in favour of high‐tech manufacturing and services.

Particularly in Western countries, those focusing on these trends have been involved in a debate about an ongoing process of ‘de‐industrialisation’, originating in the 1970s.6 By the end of the 1980s, many American and European experts had come to believe that their countries’ industries were being ‘hollowed out’ as many basic production activities relocated to other areas.

The policy consequence drawn from this development is the well‐known objective of making the EU the world’s most competitive knowledge‐based economy. How this objective can be reached has been widely debated, however, with policy makers focusing especially on an important target indicator selected to reflect the goal, namely that the EU should achieve an R&D to GDP ratio of 3%. This political and economic objective has been strongly identified with the promotion of high‐tech, high‐R&D industries.

These arguments are interlinked with a well‐known indicator measuring the ratio of R&D expenditure to turnover for a company or a business sector.7 According to the OECD categories, industrial sectors can be classified as shown in Table 1.

| High‐tech industries | R&D/Turnover > 5% |

|---|---|

| Medium‐high‐tech industries | 5% > R&D/Turnover > 3% |

| Medium‐low‐tech industries | 3% > R&D/Turnover > 0.9% |

| Low‐tech industries | 0.9% > R&D/Turnover > 0% |

High‐technology sectors (‘high‐tech’) are those with an R&D intensity of more than 5% and sectors with complex technology (‘medium‐high‐tech’) with an R&D intensity between 3 and 5%. Industries which are not research‐intensive (‘medium‐low‐tech’ and ‘low‐tech’) have a R&D intensity below 3% and are here referred to together as low‐tech and medium‐low‐tech (LMT). Pharmaceuticals, the electronics industry, motor vehicles, the aerospace industry as well as mechanical engineering, for instance, are categorised as high‐tech or medium‐high‐tech. By contrast, the LMT category includes ‘more mature’ industries such as the manufacture of household appliances, the food industry, the paper, publishing and print industry, the wood and furniture industry and the manufacture of metal products—such as the foundry industry—as well as the manufacture of plastic products (Table 2).

| R&D intensitya for aggregate of 12 OECD countriesb | 1991 | 1995 | 1999 |

|---|---|---|---|

| High‐technology industries | 9.4 | 9.2 | 8.7 |

| Aircraft and spacecraft | 13.9 | 16.2 | 10.3 |

| Pharmaceuticals | 9.4 | 10.6 | 10.5 |

| Office, accounting and computing machinery | 10.9 | 7.5 | 7.2 |

| Radio, TV and communications equipment | 7.9 | 7.7 | 7.4 |

| Medical, precision and optical instruments | 6.6 | 7.7 | 9.7 |

| Medium‐high‐technology industries | 3.1 | 2.9 | 3.0 |

| Electrical machinery and apparatus, n.e.c. | 4.2 | 4.0 | 3.6 |

| Motor vehicles, trailers and semi‐trailers | 3.7 | 3.5 | 3.5 |

| Chemicals excluding pharmaceuticals | 3.4 | 2.8 | 2.9 |

| Railroad equipment and transport equipment, n.e.c. | 2.9 | 2.6 | 3.1 |

| Machinery and equipment, n.e.c. | 1.9 | 2.0 | 2.2 |

| Medium‐low‐technology industries | 0.9 | 0.8 | 0.7 |

| Building and repairing of ships and boats | 0.9 | 0.9 | 1.0 |

| Rubber and plastics products | 1.0 | 0.8 | 1.0 |

| Coke, refined petroleum products and nuclear fuel | 1.2 | 0.9 | 0.4 |

| Other non‐metallic mineral products | 1.0 | 0.8 | 0.8 |

| Basic metals and fabricated metal products | 0.7 | 0.6 | 0.6 |

| Low‐technology industries | 0.3 | 0.3 | 0.4 |

| Manufacturing, n.e.c.; Recycling | 0.5 | 0.4 | 0.5 |

| Wood, pulp, paper, paper products, printing and publishing | 0.3 | 0.3 | 0.4 |

| Food products, beverages, and tobacco | 0.3 | 0.3 | 0.3 |

| Textiles, textile products, leather and footwear | 0.2 | 0.3 | 0.3 |

| Total manufacturing | 2.5 | 2.4 | 2.6 |

| Notes: a R&D intensity defined as direct R&D expenditures as a percentage of production (gross output), calculated after converting countries’ R&D expenditures and production using GDP PPPs.b United States, Canada, Japan, Denmark, Finland, France, Germany, Ireland, Italy, Spain, Sweden, United Kingdom.Sources: OECD: ANBERD and STAN databases, May 2003; OECD Science, Technology and Industry Scoreboard 2005, Annex A, p. 183, OECD 2005 (modified). |

In this debate, the fact that all industrialised countries have a large proportion of LMT industries, and the fact that these industries (whatever their vintage) provide goods and services that are absolutely vital to the functioning of modern societies (cf. Section 4) are often simply ignored. In spite of growing global competition, particularly in the sectors of traditional and mature industries, this continues to hold true for the industrialised countries of Western Europe as well as for the transition economies of Middle and Eastern Europe.

Further evidence for the importance of the LMT sector is provided by a number of empirical findings which emphasise the innovative ability of the low‐tech sector, particularly in high‐tech countries.8 Thus The Economist has referred to ‘the strange life’ of low‐tech industries in high‐tech California.9 From the perspective of economic history, one can argue that low‐tech industries were among the pioneers of multi‐divisional modes of organising the production and distribution of a continuous flow of branded goods. Hence, we agree with Mendonça and v. Tunzelmann10 that, ‘Innovation in low‐tech industries should … not be seen as a contradiction in terms’.

The basic research questions which pose themselves are therefore:

- •

What are the reasons for the remarkable long‐term stability of LMT sectors in the industrialised countries?

- •

Can LMT sectors be called innovative and is there a specific mode of innovativeness of non‐science based companies?

- •

What policy recommendations for the promotion of LMT flow from the factual record and sound analysis?

3. Research Objectives and Methodology

PILOT’s research on LMT industries has aimed at deepening the understanding of the growing knowledge intensity characterising economic and social development in Europe. A central assumption was that this process does not depend exclusively on industries with frontline technological knowledge but also on LMT industries. The hypothesis is that these are not necessarily low‐growth industries; many companies and branches within these industries are growing fast in comparison to the rest of the economy, are interlinked with high‐tech and service branches, and provide an important basis for future growth and employment.11 The role and importance of these industries in different European nations and for the economic and social prospects of Europe as a whole have been analysed by the project consortium.

The research objectives of the project were:

- •

to determine the role and importance of specific LMT sectors in the context of economic development in general;

- •

to identify the organisational and societal preconditions and mechanisms that enable innovation and knowledge creation in LMT industries;

- •

to ascertain the relevance of firm‐level knowledge from a network perspective in order to gain an understanding of innovative ability along whole value‐chains, including high‐tech and service companies;

- •

to contribute to the formulation of policies on industrial restructuring which pay appropriate attention to the significance of LMT industries for the further economic and social development of Europe.

To achieve these project objectives, we have used a mix of different statistical and case study‐oriented methodologies. In the process, we have tackled conceptual, taxonomic and statistical data issues and subjected a sample of low‐tech firms to detailed empirical scrutiny. The core of the project was the generation of an extensive series of 43 company case studies in 11 countries across Europe (see Table 3).

4. The ‘Strange Life’ of Low‐tech

Generally, and not surprisingly, PILOT’s statistical findings reveal the well‐known picture of economic development in all mature industrial countries.12 There is a clear trend for manufacturing’s share of total employment to decrease rapidly and for that of the service sector to increase just as—if not more—rapidly. In the period 1981–99 the share of services in employment grew strongly, from 60.7 to 70.5% of total employment in 15 OECD countries. The largest shares of growth in services occurred in two broad areas: financial services, and community and social services (the latter including such activities as health care and education). During the same period, manufacturing employment declined from 21.8 to 16.7% of total employment.

However, if one examines the industrial sector more closely, some surprising findings arise with regard to the significance of the LMT sectors. The data show that the LMT industries play a very important role in employment in all industrialised countries (Figure 1). LMT industries account, roughly speaking, for over 60% of employment in the whole manufacturing sector whereas the share of high‐tech industries is less than 10%. There has been a tendency for the low‐tech industries’ share of manufacturing to decline during the long period 1980–99, while the share of high‐tech industries has increased. A similar trend can be observed regarding the share of value added of the different sectors in manufacturing. In the long run, starting from a low level, high‐tech sectors show a rising share of the value added in manufacturing while the share of the LMT sectors is declining. However, these declines are not marked, and the LMT industries still constitute by far the largest part of the manufacturing sector in OECD economies. It is debatable whether there is a real structural change in the period examined here. In fact, the low‐tech sectors continue to evince remarkable stability and a high share of employment (Figure 1).13

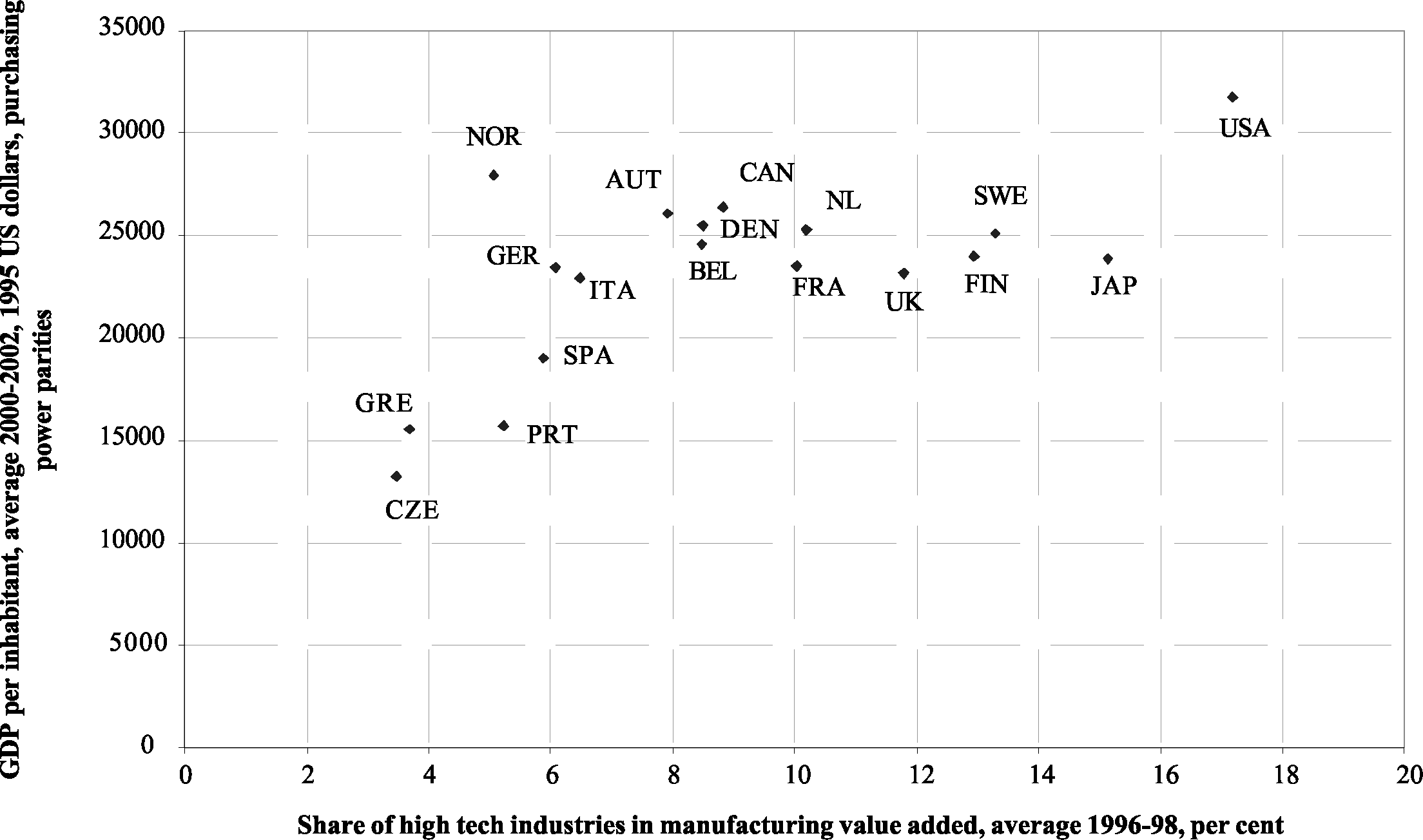

In addition, there is no clear connection between high technology intensity and national growth rates. The question is whether countries with a higher share of high‐tech sectors have better overall growth records. On the basis of the statistical data, no positive correlation can be found between the high‐tech share in manufacturing value added and the rate of growth of GDP per inhabitant. This is illustrated in Figure 2.

GDP per capita. Average 2000–02, 1995 US dollars (y‐axis); share of high tech industries in manufacturing value added. Average 1996–98 (x‐axis).

Furthermore, it is wrong to conclude that only high‐tech countries are also high growth countries. Rather, it is clear that, even in the EU, many low‐tech countries have impressive growth rates. All our findings lead again to the question: what are the reasons for this remarkable stability of LMT industries? The answer requires a discussion of the mode of innovation in non‐science based industries.

5. Mode of Innovation

A central precondition for the surprisingly high strong performance of the LMT industries is their strategic flexibility and ability to innovate. These enable them to face up to the pressures of world market competition by developing new products, new process technologies and new ways of organising. For a better comprehension of this connection, it is essential to come to an understanding of innovation processes that a narrow focus on R&D intensity obscures. In order to deal with this issue, PILOT has focused on the central dimensions and mechanisms that underlie the innovation ability of firms in LMT sectors.

5.1. Basic Dimensions

The starting point of our analysis is the argument that the dominant concepts developed so far to describe and analyse industrial and technological change have many shortcomings. Our main argument is that it is wrong to interpret innovation processes as a linear process. The linear model assumes that research and development activities are the starting point of any kind of innovation and that scientifically generated knowledge is a prerequisite for the development of new technologies. If firms with low or no R&D—i.e. most LMT firms—are innovative, then the linear model should not be accepted as the basis for debates on innovations. A more theoretically based criticism refers to Joseph Schumpeter’s concept of innovation.14 This concept establishes no compelling connection between innovation and scientific or technological originality at all. All creative activities which contribute to diversity and thus generate profits count as innovations in Schumpeter’s concept. Many of the problems faced by today’s innovation researchers, such as classifying the ‘uniqueness’ or ‘technology height’ of innovations, are of little relevance from this perspective. What matters is not the existence of a science base but professional creativity that can score in the marketplace. Schumpeter’s formulations allow for a better understanding of the creative processes which take place in so‐called low‐tech manufacturing sectors as well as in many service sectors, including those labelled knowledge intensive business services.

Following this basic idea, an analysis of LMT innovation processes may start by asking how successful companies manage to develop or create the capabilities and competencies which make them perform better than their competitors or at least help them to survive commercially. Part of the answer may, of course, be found in R&D activities or in what can be identified as R&D (the two are not necessarily the same), carried out and financed in‐house or acquired from outside sources. Another part may be related to other activities, of which some may be called innovations and others may be a far cry from what innovation researchers normally focus on. A convincing analysis has to identify and capture all these ‘profit enhancing’ or ‘survival facilitating’ activities irrespective of their labelling. To analyse the requirements and preconditions for the innovativeness of low‐tech companies more closely, it is therefore necessary to clarify the specific structural conditions of these firms. These can be characterised relatively precisely by recourse to the R&D intensity indicator: the companies have limited or no independent R&D capacities at all and their in‐house expenditures on, for example, R&D personnel and other costs and investments connected with R&D activities are low. Their outside spending on R&D by other companies or organisations is likewise small. As a result, one can assume that these firms have other kinds of resources and capacities to act, on which their innovation ability is based and which (functionally) compensate for their lack of R&D capacity.15

5.2. Capabilities

A possible starting point for such an analysis could be resource‐oriented analysis concepts of innovation and management research16 which lend themselves well to attempts to specify the connections we are considering. These concepts aim at examining how firms attain competitive and innovative advantages, what resources they have at their disposal in this respect and how they employ these resources. The central argument is that companies can be characterised by means of their specific combination of more or less special and rare resources, especially of knowledge in miscellaneous forms and not only of R&D based scientific knowledge. Furthermore they must apply a specific competency or combination of competencies to be able to make use of these resources for their strategic goals in each case. The dynamic capabilities approach of Teece et al.17 elaborated more recently by Zollo and Winter,18 is relevant in this context because it provides a framework for examining the broad variety of firm‐specific factors that are important for explaining innovations. Design and synthesising capabilities can be especially significant in this respect.

To be able to analyse these connections and the mechanisms linking available resources and innovation outcomes of diverse kinds more precisely, a specification of the capabilities approach is needed. Bender and Laestadius19 provide this by suggesting that the term capabilities should not be understood as a pattern of activities but rather as a term to address specific preconditions for specific activities: a particular configuration for enabling the cognitive, financial and material (machinery etc.) resources that an organisation possesses. They further suggest two fundamental dimensions, namely transformative and configurational capabilities. The former focuses on the enduring ability of an organisation to transform externally available, codified knowledge into company‐specific knowledge, the latter on the enduring ability to synthesise novelty by creating new configurations of knowledge, artefacts and actors. Three specific aspects of configurational capabilities may be distinguished:

- •

cognitive: configuring distributed knowledge of different kinds;

- •

organisational: configuring distributed actors and other repositories of knowledge and know‐how; and

- •

design: configuring functional features and solutions.

The distinction between transformative and configurational capabilities is analytical; empirically the two dimensions are tightly interwoven.

Innovation in the LMT firms and sectors that we have examined is to a great extent the result of the transformation and reconfiguration of well‐known internal and external knowledge and of components and technologies developed elsewhere. What all the case firms in this sample had in common was that not one of them based its innovativeness on recent scientific findings and knowledge. The conclusion of this analysis is that, even within mature industries with unfavourable cost conditions, at least some firms may develop capabilities which make them profitable and competitive over a relatively long period. In these cases, innovation is to a great extent the result of processes of transforming and configuring generally well known knowledge, components and technologies developed elsewhere. There may also be knowledge formation processes similar to what can be found in other firms labelled as high‐tech or medium‐high‐tech. In general, this approach to ‘innovation enabling capabilities’ developed in the context of the PILOT project, is not only appropriate for the analysis of innovation processes in LMT industries but may also be useful for science‐based innovations.

6. Practices and Resources

6.1. Knowledge Management and Personnel Policy

The concept of capabilities refers to the conditions on which an enterprise’s ability to be innovative depends. This issue can be addressed by looking at the findings of innovation studies. According to these, one can basically start from the assumption that this ability is strongly embedded in the practices and processes of the firm’s organisation.20 Following Schmierl and Köhler,21 these include the modes of knowledge management and personnel policy used by a firm as central elements of transformative capabilities in LMT companies. According to the case studies findings, there is neither one common pattern regarding workforce and work organisation nor one shared pattern of knowledge creation and utilisation. The knowledge base of the low‐tech companies investigated can be characterised as ‘accumulated internal knowledge’. Regarding the processes of knowledge creation, two main, opposing, patterns were identified:

- •

the stimulation of collective accumulated knowledge on the shop‐floor; and

- •

the concentration of knowledge creation in the hands of specialised personnel in the planning departments in terms of a Taylorist tradition of work design.

Both patterns are characterised by a systematic combination of dispersed knowledge and an incorporation and assimilation of external knowledge. It can be shown that LMT firms are not basic innovators but combine existing codified knowledge with practical knowledge in a competitive way. The knowledge management strategies which can be identified are not at all different from other sectors although there was one frequently expressed position: ‘We are followers, not trendsetters’. LMT firms very often improve their ability to incorporate external knowledge which has already been implemented and tried by others. Benchmarking and learning from the best is a very common practice which requires the capability to observe, to obtain information, to analyse and to transform machines, design or organisational structures from other contexts.

As regards work organisation and personnel policy, many low‐tech companies are characterised by specific capabilities in processing technology and logistics which produce uniqueness and competitiveness. The case study sample ranges from companies using ultra‐modern machinery and highly automated processes (especially in the paper industry, but also in parts of the metal‐working industry) to companies which are barely automated and still depend for the most part on traditional manual labour and standard technology (as in the food, textile and wood processing industries). However, as a general rule, it can be emphasised that the term low‐tech as a classification of sectors is not necessarily synonymous with low‐tech manufacturing processes.

The same holds true for patterns of work organisation.

- •

The workforce and work organisation vary from company to company. This means that there is definitely no low‐tech specific pattern of work organisation and qualification levels which is systematically distinct from medium‐ or high‐tech sectors. This heterogeneous economic segment is instead characterised by a variety of different forms of work organisation.

- •

Concrete patterns of work organisation are determined by an interplay of many factors, such as product complexity, production process characteristics and automation, personnel policy, quality requirements and customer demands. There is also a wide variety of qualifications and skills with differences as to where and in what form transformative capabilities are located internally.

- •

Most firms, however, are characterised by the concentration of strategic knowledge in the hands of a rather small group of managers and technical staff while the production workers are more or less skilled operatives.

The dominant patterns of personnel policy rely heavily on the predominance of internal training, which is mostly supplied unsystematically during daily work and at the workplace. In most cases, forms of vocational further training predominate with a great range of intensities. Apart from characteristic differences (e.g. between the sectors or certain types of enterprises), Schmierl and Köhler22 found three predominant basic modes of vocational education and training in the sample. In order of importance, these are:

- •

internal training on the job and learning by doing;

- •

recruitment of key workers on the external labour market followed by an internal phase of training on the job; and

- •

cooperative further training with other institutions and companies.

To summarise the PILOT findings with respect to knowledge management and personnel policy in the investigated low‐tech companies, the regular workforces of many companies hold a considerable, as yet underdeveloped, potential for the improvement of transformative capabilities which can be tapped by strategic training and by improved and appropriate forms of work organisation. As the authors emphasise, most of the low‐tech companies investigated seem to follow a policy of ‘muddling through’ instead of a systematic and foresighted personnel policy.

6.2. Networks and Local Embeddedness

Network relations between companies and supportive social networks are becoming increasingly important for the capacity of LMT industries to act, given the growing challenges of the world market and globalisation. This is the basic argument of Garibaldo and Jacobson,23 whose systematic analysis of the empirical findings concludes that:

- •

the equation ‘low‐medium‐tech industry = locally embedded processes’ is not tenable; while some of the businesses studied are highly embedded, others are not; and

- •

likewise, the equation ‘low‐medium‐tech = structural weakness in the face of globalisation’ is wrong. Some of the study cases provide evidence of strongly embedded processes but nonetheless proved able to attain a global market position.

Many of the cases investigated concur with overall business trends towards increasing internationalisation. For many LMT firms, an increase in internationalisation has meant a decrease in territorial embeddedness. What is significant, though, is that a number of the firms have successfully increased their level of globalisation while simultaneously maintaining a high degree of local embeddedness. In these cases, the research findings substantiate the connections well‐known from earlier regional research—that firms in general, but especially LMT firms, are very sensitive to the density of the institutional set‐up both on the national and sub‐national levels. ‘Density’ in this case stands for a mix of physically available infrastructures, of educational and vocational knowledge creation, and of diffusion and brokerage facilities. Thus there is no typical LMT firm characterised by standard behaviour concerning global or local orientation strategies. On the contrary, there are close interdependencies between these factors.

In this context, the aspect of the integration of LMT firms into value chains is also of strategic importance, especially in the light of a progressive restructuring process of value chains. The empirical findings show that LMT firms are distributed at different levels so that there is no single formula for success. LMT companies often play a strategic role in the smooth functioning of value chains. It is not surprising that proximity is important in this regard. However, this does not necessarily mean spatial proximity. More important are forms of cultural and organisational proximity that constitute the precondition for the passing on of knowledge (especially practical, non‐codified knowledge) between companies. Again the social context is of critical importance for technological evolution and innovative capacity. In many cases, value chains as well as clusters need strong intermediate institutions and institutional infrastructures to provide resources for the management and organisation of networks. Such institutions can be created through the combined efforts of public institutions and local stakeholders so that social contexts can be generated that strengthen the innovation process. Where LMT firms are otherwise excluded from innovative networks, this process can lead to their inclusion.

6.3. Interrelationships of Low‐tech with High‐tech Sectors

As shown above, the term low‐tech as a classification of sectors is not necessarily synonymous with low‐tech manufacturing processes. Therefore both the ability to integrate and to utilise high‐tech manufacturing technologies and the relationship of low‐tech to high‐tech sectors are of decisive importance for the development perspectives and prospects of LMT companies.

However, as the PILOT findings show, technological flows do not move only from new and higher‐technology sectors to older and lower‐technology sectors. The analysis of the interrelationships between LMT companies and high‐tech companies within value chains clearly show the strategic role LMT companies play for innovation in high‐tech.24 In different cases it could be recognised that LMT companies actually boost the innovative capabilities of high‐tech firms. In the case of the paper industry in Germany the main impulse for innovation typically comes from the paper manufacturer’s request that the chemical supplier, a high‐tech company, should either alter an already existing product or develop a new one (e.g. a new dye). The fostering of innovation in high‐tech companies by LMT firms is also illustrated by an Italian case on the value chain for sintering. In this case a die manufacturer, which is formally defined as a low‐tech company, is involved in continual product innovation and is able to influence the design processes of its high‐tech clients.

Furthermore, Robertson and Patel25 emphasise that in many cases the viability of high‐tech sectors and the levels of resources devoted to research and development are directly related to the rate of diffusion because the main customers for high‐tech products are in the LMT sectors, and therefore the rates of return to R&D in high‐tech areas are a direct function of rates of technological diffusion. For Robertson and Patel26

perhaps the most important backward linkage from LMT to high‐tech industries comes simply from the revenue that sales provide, which helps to cover the substantial fixed costs that arise out of the innovation process and engenders economies of scale. In innovative situations, lumpiness and resulting non‐convexities affect several areas including gearing up for production and the expenses associated with R&D itself. Diffusion can be crucial at this stage because the larger the number of LMT industries that adopt an innovation, the quicker the rate of amortisation of development costs will be. These economies of scale can then be translated into lower prices of innovative products for the LMT industries (greater pecuniary externalities), further economies of scale for the high‐technology industries, and the generation of what Nurske27 has termed a ‘beneficent circle’.

This relationship between high‐ and low‐tech industries is depicted in Figure 3.

The project findings emphasise that future industrial development in Europe does not depend on making a choice between high‐tech and LMT industries. Rather, the performance of all these sectors is inextricably linked. While the productivity of LMT sectors is based on high‐tech innovations, the innovative capability of the high‐tech sectors also depends on their narrow relationship with LMT industries.

7. Policy Issues

One of the main objectives of the PILOT project has been to make policy recommendations for the promotion of LMT sectors. On the basis of the research findings of the project, Jacobson and Heanue28 have identified a number of significant factors and problem situations concerning innovation policy for LMT sectors.

7.1. Limited Awareness of LMT Industries

Referring to the EU in general, our empirical findings show that there is little if any awareness of innovation‐generating policies other than those focusing on R&D. Correspondingly, the low‐tech sectors receive little attention from innovation policy makers on different levels, such as the EU, the national state and the regions. Therefore, a key policy task is to support activities and measures raising the awareness of low‐tech industries and their specific needs and conditions. A fundamental precondition for this is the development of a new and broad understanding of innovation and the insight that one should no longer equate innovative ability with R&D activities alone. The more recent debate within the Commission and the OECD about the need for new R&D indicators certainly points in the right direction and should be intensified.

Such intensification might include the establishment by the EU of a mechanism to closely investigate the needs of LMT firms so as to identify ways of supporting innovativeness. Whatever means are identified to provide support must be flexible enough to correspond to the objective and cultural needs of the recipients. The problems of differences in Europe in the attitudes of entrepreneurs, which were especially prominent in Polish case studies, underline why such institutional flexibility is essential.

PILOT research suggests that Polish and other new member LMT firms may have an importance that extends beyond their immediate geographical contexts and across the EU as a whole. There is a need to examine this more closely and to research the potential for integrating the capabilities of Central and Eastern European firms into the dynamic of the Union, rather than de facto treating these companies as dinosaurs destined for extinction as a result of natural selection. A further fundamental prerequisite is a holistic view of industrial innovation processes and the relevant interlocking of different kinds of knowledge as well as of the different elements of the companies’ capabilities which enable them to be innovative and profitable. The policy conclusion to be drawn would therefore be that it is necessary to focus on the industrial innovation chain as a whole, to concentrate more strongly on inter‐sectoral connections and to make a point of finding the potentials of low‐tech industries.

However, it must also be emphasised that the firms themselves have a low level awareness of innovation policies for LMT industries and that policy measures are perceived very differently by different firms. The policy measures that are regarded as helpful by some firms as a rule concern general aspects such as national policies providing tax incentives and subsidies for various activities and EU policies such as the Framework Programmes and Eureka. On the whole though, one can state that there are great innovation policy shortcomings as far as the specific problem situations of LMT companies are concerned.

7.2. The Relevance of Knowledge and Company Capabilities

As for the knowledge base, low‐tech innovations presuppose the availability of specific practical in‐house knowledge as well as the integration and use of complex knowledge inputs within networks. It is therefore an important policy task to conceive measures and to support activities which aim at improving the knowledge base and capabilities of low‐tech companies. This task can be realised at both the level of EU‐wide support programmes and also at national and regional levels. In practice, such measures should be directed at promoting the different dimensions of, and particularly the preconditions for developing the capabilities of, LMT companies. The organisational conditions and management skills regarding a more efficient use of existing knowledge are especially in need of further development.

In this context a key problem relates to training and recruitment needs. The necessary training for the array of skills required by workers in the LMT companies is not readily available from mainstream providers. Standard qualifications do not provide the mix of skills that LMT firms require. Additionally, many of the firms are experiencing recruitment difficulties due either to the negative image of the industries or to skills shortages.

7.3. Local Embeddedness and Network Relations

Policy tasks should focus on the development of the companies’ organisational structure so that they are geared to the demands of cross‐company co‐operation with corresponding channels of communication, gateways and personnel responsibilities. In this respect, the professionalism of management of LMT firms should be supported and further developed. Another important policy task is to concentrate on improving the firms’ capabilities for making the right strategic choice as regards the dilemma between globalisation and local embeddedness. The findings of the PILOT project show the importance of a balanced dynamic between global, local and regional policies that operate in all sets of ‘environments’ to which a firm may belong; the aim of policies at different levels to create infrastructure supporting the innovation process must facilitate this balanced dynamic. Clusters and fragmented economies need strong intermediate institutions and institutional infrastructure to provide appropriate local conditions. To set up such institutions, the positive combination of the vision of public bodies and the interests of the stakeholders (i.e. collective actors) are important factors.

7.4. Interrelationships of Low‐tech with High‐tech

A key policy question underlying the PILOT project was whether European innovation policy should focus on so‐called high‐technology and science‐based industries in attempting to solve growth and employment problems, or whether it should look to the growth prospects within the low‐ and medium‐technology industries on which the European economy is actually based. An important PILOT result is a recognition that the policy issue is not a choice between these apparent alternatives.

The PILOT project showed that the vast majority of output and employment in modern economies is accounted for by both manufacturing and service LMT sectors. Such sectors are also significant users of the output from high‐tech sectors. In a modern economy, the levels of performance of both high‐tech and non‐high‐tech sectors are heavily interdependent, and policy should view the economy as a whole. As a result, the promotion of the 90% of the economy that is made up of LMT sectors also promotes the welfare of the high‐tech sectors.29 As a corollary, policies need to ensure that they encourage both the generation of knowledge and its diffusion, and that both operations are carried out at high velocity to maintain competitive advantage.

Before formulating specific policies, however, the EU needs to establish a mechanism to closely investigate the needs of LMT firms and the thought processes and aspirations of entrepreneurs and managers. To judge from our studies, these issues are often not even on the radar screens of Commission bureaucrats and policies are often made in vacuo from an informational point of view. Moreover, institutions for delivering help need to be designed so that they correspond to the objective and cultural needs of the intended recipients. Policy makers need to inform themselves on the factors that managers feel to be important, rather than hypothesising motivations, and target their recommendations to elicit positive responses given the psychological make‐up of entrepreneurs and other managers. For example, there is considerable evidence that many owners of SMEs prize their independence and do not greatly value advice from governments. To deal with this, policy makers need to consult the views of what owners and managers regard as significant when launching institutions to improve innovation among LMT firms.

8. Development Perspectives of LMT in the European Union

Finally, the following should be emphasised: in spite of the doubtlessly difficult economic situation of LMT industries and the challenges of globalisation and growing competition in the world market, prospects for many LMT sectors and companies are reasonably promising, even in countries with advanced economies. This is true for a number of reasons.

- •

Firstly, the specific competences which many low‐tech companies possess cannot easily be copied by potential competitors because they are deeply embedded in the social system of a company and its local environment, which makes them difficult to transfer and thus fairly inaccessible to competitors.30 This—paradoxically—applies to standardised products which are usually considered easy to imitate, but such products are often design‐intensive and have major potentials for technological upgrading via the use of complex knowledge inputs.

- •

Secondly, the geographical and social proximity to sales markets and specific customer groups as well as the capabilities of many LMT companies to use and influence these advantages in a flexible manner, are a further important reason for the relatively favourable development perspectives of such companies. For low‐cost competitors from other countries, on the other hand, it is often a time‐consuming and difficult task to establish the necessary contacts and to gain the required information.

- •

Thirdly, a considerable number of low‐tech companies are obviously in a position to employ high‐tech process technologies systematically and efficiently. Their specific process skills, and frequently also their well‐established contacts to the manufacturers of such technologies, form the basis for this achievement. Quite evidently the high‐tech environment is a central requirement for the development perspectives of low‐tech enterprises in this case.

These considerations should lead to a new understanding of the restructuring of the economic landscape of Europe in the first years of the twenty‐first century. The economy does not appear to be undergoing a wholesale structural replacement of ‘old’ sectors with ‘new’ ones, or a substitution of ‘old’ technologies with ‘new’ ones. In fact, this process of change is evolving as a restructuring of sectoral and technological systems, transformed more from within than from without. It is not dominated by industrial activities for which competitive advantage, capability formation and economic change are generated by front line technological knowledge. Rather, it is dominated by what are often wrongly termed low‐ and medium‐tech industries. And it is characterised by a specific combination and continuous re‐combination of high‐ and low‐tech.

On this note, it has to be emphasised again that industrial innovations are, for the most part, not based on newly created scientific knowledge. Even where technical change is based on scientific activities, it is not necessarily based on recent ones; innovations stemming from the stock of knowledge and the solution of practical problems of various types may be more important than the creation of new knowledge. The relationship may, in addition, be the other way around, i.e. technology creating the foundation for scientific knowledge.31 LMT industries are well placed to play a decisive role for innovations because the contribution of LMT companies is frequently an important precondition both for the innovativeness of value chains—or production systems—and for the design, fabrication and use of a range of high‐tech products. As is convincingly shown by Robertson and Patel,32 the relationships between high‐tech and non‐high‐tech sectors in developed economies are highly symbiotic and the well‐being of high‐tech firms and industries depends heavily on their ability to sell their outputs to other sectors in developed economies.

Collaboration and networking between companies of different industries at regional, national, and transnational levels are increasingly important determinants of the innovativeness and competitiveness of individual companies. These value chains, filières or clusters include low‐tech companies not just as third tier participants in supply chains or as more or less passive recipients of technologically advanced machinery and equipment developed independently of user specifications. Furthermore, the dynamics and efficiency of value chains may crucially depend on the reliability and effectiveness, the capabilities and specific knowledge of their low‐tech partners and on their integration into innovation processes in other firms in the cluster, whether low‐tech or high‐tech.

This focus on the contribution of low‐tech industries to the innovativeness of industry as a whole is extremely important from a policy perspective, both at national and regional levels. It is indispensable for developing a proper foundation for the overall growth and performance possibilities of the European economy. Following the above line of argument, the high‐tech prospects of many economies are based on the presence of and dynamic interaction with reliable low‐tech functions and processes. The significance of low‐tech companies as regards innovation policy must ultimately also be seen against the background of the strong and probably increasing international competitive pressure on complex technologies and products. Their market position can by no means be regarded as permanently stable and promising. High technologies and the corresponding know‐how can, in the context of global economic integration, diffuse rapidly. And the crucial point is they are also quickly utilisable for innovations, so that the window for realising innovation profits in this sector is in many cases quite small. One instructive example, as experts stress, is that a developing country like China will in some years be one of the largest developers and producers of high‐tech products such as mobile phones. Another example is the situation of the medium high‐tech automotive industry in countries like Germany. It is occasionally pointed out that the dependence of German manufacturing on the auto industry provides specialisation advantages but that it also increases the risk of severe damage from competition as highly sophisticated cars are increasingly being produced more cheaply in newly industrialised countries (albeit often by German firms). The policy conclusion to be drawn would therefore be that it is necessary to focus on the industrial innovation chain as a whole, to concentrate more intensely on inter‐sectoral connections and to make a point of identifying the potentials of low‐tech industries. Most notably, the empirical findings show that there are favourable development potentials for low‐tech industries, not least in the high‐tech‐oriented countries of the European Union.