Introduction

Financialization has been a popular leitmotif in contemporary heterodox economic analyses since the 1990s. Its main thesis is that finance has become the center of gravity of the capitalist economy and subsequently transformed the whole system according to its prerogatives. This is a novel proposition and contradicts the previously held assumption of almost all economic traditions; namely, that the “real” economy (the producing sector) is the center of the economic circuit and the financial system is a necessary but subordinate activity. Needless to say, if this financialization hypothesis (FH) holds, then the whole modus operandi of the capitalist economy (the class structure and its composition, the relationship between production and circulation, the source of profits, etc.) alters radically.

However, popularity and novelty do not necessarily bestow wisdom. Mavroudeas and Papadatos (2018) disputed FH’s analytical and empirical validity. They have argued that the post-1990s financial expansion is not a historically unprecedented phenomenon, apart from certain significant but not crucial specific features. On the contrary, the expansion of the financial sector is a usual case during the beginning of economic downturns. Moreover, they argued that the argument that the financial system has acquired a new and separate source of profits (which is popular within FH tradition) is groundless. Hence, finance’s divorce from production is unsubstantiated. Finally, they argued that FH’s ambitious proposition that financialization constitutes a new stage or type of capitalism fails to account realistically for the evolution of contemporary capitalism. This article extends this analysis and provides further challenges to FH’s analytical and empirical validity.

The article is structured as follows. The next section deals with the definition of financialization. The popularity and widespread use of the concept have led to increased vagueness as different authors and theoretical streams ascribe it to quite different content. This is a major problem that undermines a major part of the literature and renders them futile. Clarifying the existing ambiguities of the concept, therefore, is a good starting point.

The theoretical section analyzes the birth, evolution, and basic currents of the FH. It offers a critique of the FH and rejects several of its major arguments. It argues that financialization does not constitute a new stage or type of capitalism and that such arguments fail to accurately account for the evolution of contemporary capitalism. Finance has not acquired an autonomous existence and a separate source of profit from productive-capital or dominated it. Divorcing finance from production, therefore, is unsubstantiated. Finally, it argues that, apart from certain significant but not crucial specific features, the post-1990s financial expansion is not a historically unprecedented phenomenon. On the contrary, it is usual for the financial sector to expand at the onset of economic downturns.

The empirical section scrutinizes and disputes several specific empirical arguments maintained by several authors of FH. It shows that (a) the big majority of the largest multinational companies are not financial firms, (b) there is not an abnormal increase in the ratio of financial assets to economic activity during the recent decades, (c) financialization is not the main cause of deindustrialization, and (d) financialization does not originate from financial liberalization. It is important to emphasize that the empirical part does not refute all the empirical claims cited in the financialization literature. It aims to dispute only the aforementioned four fundamental arguments which are clearly stated by several influential authors.

The last section concludes by highlighting the main findings of the article.

Defining Financialization

The study of the FH stumbles upon several pre-analytical obstacles as serious differences exist between the different FH variants. The proliferation of the term worsened this as it became a fashion employed by many with widely different meanings and contents. This made financialization a fuzzy concept. Even the propagators of the term recognize it as a “concept in search of a theory” (Bryan, Martin, and Rafferty 2008, 122). This lack of theoretical clarity seriously hinders FH’s analysis as its fluidity makes it difficult to pinpoint its substance.

The first problem concerns the theoretical domain of financialization. Even erudite authors (e.g., Fine 2014) consider financialization as the exclusive property of heterodox economics. However, this is not so. Mavroudeas and Papadatos (2018) pinpointed the existence of a strong mainstream New Keynesian version and delineated three main financialization traditions (mainstream, post-Keynesian, and Marxist/Marxisant) with sub-currents. Hence, financialization does not necessarily imply a critique of capitalism.

The second problem concerns the very definition of the term. We can distinguish two polar cases regarding the definition of financialization. The initial definition considered financialization as a “structural break” in the evolution of capitalism. Thus, it emphasized four purported novel characteristics of contemporary capitalism: (1) financial sector’s increased share in GDP; (2) increased speculation and volatility, fomented by new financial instruments (shadow banking and derivatives); (3) financialization of non-financial corporations (e.g., Lazonick 2014) as shareholders’ value maximization policies and the rise of the absentee investor dictated share buybacks and short-termist investment decisions; and (4) increased households’ indebtedness.

This initial definition was further subdivided between those who argued that these characteristics are transient products of specific policies (e.g., Krippner 2011) and those arguing that they constitute a new capitalist stage.

However, a new definition was proposed with the increased popularity of financialization: it is a recurrent phenomenon that has also happened in the past. There are several versions of this view (e.g., Fasianos, Guevara, and Pierros 2016). The majority adopts Arrighi’s (1994) argument that financialization is a recurrent cyclical phenomenon in the evolution of the capitalist world system. Arrighi (1994) argues that capitalism evolves through distinct epochs. Each one of them is dominated by a hegemonic power. When an epoch is on its ascendancy the hegemonic power (and the world system as a whole) is geared to production and the real economy. When an epoch moves toward its decline, then the system is geared toward the financial system. The mechanism of this transition is the following. Arrighi employs a simplified version of Marx’s total circuit of capital (M–C–M’) and breaks it into two sub-circuits. During the ascendant phase, there is material expansion as the system exhibits cooperation (through increased division of labor) and increasing returns to capital (Arrighi and Silver 2001). Thus, more profits are being generated which are reinvested and expand the economy. This material expansion corresponds, for Arrighi, to Marx’s M–C, where money is translated into commodities through the production process. However, at some point in time, some kind of entropy seems to operate, which Arrighi fails to define adequately. Then, returns to capital (profitability) start decreasing and competition (instead of cooperation) increases. Profits are accumulated but cannot be reinvested profitably in material production. Hence, over-accumulation occurs, and this leads to financialization. The over-accumulated money-capital goes into financial expansion C–M’ (commodities generate profit through a financial expansion of the world economy). This dichotomization of Marx’s total circuit of capital is very problematic. In Marx’s view, the M’ corresponds to a C’ created in production. Hence, additional (financial) profits cannot occur by augmenting the money supply. Financial profits are a segment of the surplus-value expropriated in production. Moreover, Arrighi is vague regarding the mechanism via which accumulation goes into over-accumulation. Marx’s theory proposes a specific mechanism (based on the tendency of the profit rate to fall) for this.

There is another problem that has to do with Arrighi’s Braudelian “long-duree” view of recurring financialization. It is too long-run and thus engulfs unjustifiably quite different epochs with very diverse characteristics. For example, it equates capitalism with pre-capitalist eras (mercantilism) and, thus, loses the former’s specificity.

Finally, Arrighi faces some disconcerting contemporary empirical problems. If a weakening hegemon resorts to financialization, then how can it be explained that (a) the major financial center today is the British city (belonging to the previous hegemon) and not the US Wall Street (belonging to the current hegemon)? And (b) US debt is financed not by US capital but mainly by foreign capital (and particularly Chinese) and not by domestic funds (as the Arrighi thesis maintains)?

However, despite the abovementioned problems, Arrighi’s view that when over-accumulation occurs, a great part of this over-accumulated capital goes into the financial system and hunts for extra profits at the expense of cash-strapped productive-capital is correct and has been pointed out by Marx and several Marxist economists (e.g., H. Grossmann—see Mavroudeas and Papadatos 2018). This can expand the share that money-capital gets out from the total surplus-value extracted.

Arrighi’s argument that during the decline of a hegemonic power the latter employs its financial resources to avert its decline is also correct. Usually, a hegemonic power has strategic control of the international financial system and its mechanisms and institutions (e.g., dominant reserve currency, and international mechanisms of capital transfers). But, as the financial system exists on the back of the productive system, its “weaponization” cannot be long-lived.

Setting aside the pros and cons of Arrighi’s thesis, its adoption by many FH supporters is quite uncritical and superficial. Thus, they neglect specific features of Arrighi’s analysis that pose serious problems to his newly found disciples.

First, Arrighi adheres to the world system perspective; meaning that the global system is the basic unit of analysis and national states and policies have an insignificant analytical role. Thus, it is quite contradictory to adopt his thesis and at the same time speak about various types of financialization (national, regional, etc.).

Second, Arrighi advances a cyclical view of capitalism’s evolution and rejects stageist views. Hence, financialization cannot be considered a distinct stage within his perspective.

Third, most of FH’s four major stylized facts do not exist during Arrighi’s previous financialization phases.

To sum up, in our opinion defining financialization as a recurrent event is rather indeterminate. It ends up with a very broad and vague definition of financialization that tries to encapsulate quite different phenomena existing under very different historical circumstances.

On the contrary, defining financialization as a structural break has the merit of being more specific and bodes well with the argument that it is a new epoch characterized by a structurally different new capitalism. If the financial system has broken loose from the yoke of the productive sector and has imposed a new modus operandi on the whole system, this certainly did not exist in the past. This version of financialization argues that financial-capital is not receiving a portion of the surplus-value extracted by productive-capital but it is directly and independently receiving income by usuriously exploiting indebted households and other capital (through shadow banking and shareholders’ value-maximizing).

If financialization purports to have any significant meaning, we argue, it must be identified as a structural break; that is, as a new capitalist stage. If it is simply a transient phase of the economic cycle or related to a policy choice, then it does not deserve the attention drawn to it.

Finally, apart from the disagreements over its novelty, opinions also differ regarding whether financialization is responsible for the slowdown in real accumulation. Differences also exist on whether financialization follows a basic model (as in the US and the UK) or if there are several types of financialization. This article tackles these issues in both its first part where the different streams of the FH are presented and assessed and in its second part where fundamental empirical expectations of the FH are scrutinized and refuted.

The Theoretical Debate

The FH appeared in the 1990s when capitalism had surpassed its third global crisis (in the 1970s) only to fall into a prolonged era of weak accumulation. After several heuristic capitalist restructuring waves that produced meager results, there has been an increasing application of old and new financial instruments as a means to evade sluggish accumulation since the 1990s. Financialization has been employed within almost all major economic traditions as an explanation for this state of affairs (Mavroudeas and Papadatos 2018).

Mainstream financialization theories stem mainly from New Keynesianism and argue that new financial capitalism has emerged where finance is a major growth contributor (King and Levine 1993). They abandon general equilibrium’s aversion to a big financial sector and praise (a) the increasing role of capital markets by arguing that market-based financial systems are more efficient and less risky than bank-based ones and (b) households’ increased participation in the stock market as the democratization of ownership and shareholders’ capitalism. Based upon New Keynesianism’s endogenous money theory and the financial accelerator, they reject money neutrality and maintain that the credit market and the financial intermediaries cause economic fluctuations through the endogenous allocation of existing liquidities. Information asymmetries (adverse selection, moral hazard, etc.) cause credit-market imperfections (e.g., borrowers with strong financial backing obtain credit more readily and cheaply). Firms and households use some of their assets as collateral in borrowing activities to ameliorate these frictions. This results in an environment where external finance is more expensive than internal finance when the former is not covered by collateral; thus, creating an external finance premium. The latter affects the overall stock of capital, thereby influencing investment decisions and aggregate demand. These cause multiplier effects (through the financial accelerator) that affect output dynamics (Bernanke and Gertler 1989) and propagate and amplify shocks to the macroeconomy. On this basis, New Keynesianism explains contemporary financial phenomena such as shadow banking and repos.

Mainstream FH’s endogenous credit-money theory has well-known problems. First, it lacks a robust stages theory. Thus, when it considers financialization as a new stage, it views it as a chance event rather than being able to relate it to the main functions of the capitalist system. Finally, because it has a non-social perspective (it does not recognize social classes) it has a limited explanatory ability.

In heterodox economics, the FH was introduced by the Monthly Review (MR) School. However, soon post-Keynesianism adopted the term (Stockhammer 2004; Hein 2013) and even treated it as its own (van Treeck 2008). Both currents acknowledge Minsky’s (1992) Financial Instability Hypothesis as their forerunner.

Post-Keynesians often place financialization within a stages theory and argue that new finance-dominated capitalism (Hein 2013) emerged at the end of the 20th century. In this stage, the financier assumed primacy over the industrialist. Their analysis dichotomizes capitalists into two separate classes: industrialists and financiers with opposing interests. Post-Keynesians argue that the advent of neoliberalism in the 1980s empowered the financiers over the industrialists and caused a tremendous increase in financial leverage and financial profits at the expense of slowing investment and growing instability. This resulted in the 2008 crisis, which is considered a purely financial one. The post-Keynesian remedy is a return to prudent Keynesian regulation to stabilize capitalism. In analytical terms, the post-Keynesian FH is founded (similarly to New Keynesianism) on a theory of credit-money created endogenously via the operation of the banking system. Moreover, several post-Keynesians consider endogenous money primarily as endogenous finance (Wray 1992; Toporowski 1999). Hence, the interaction between financial and goods markets includes wider forms of finance and not only bank-credit.

The post-Keynesian FH endogenous credit-money theory cannot coherently define what is capital. Consequently, it misconstrues the relation between interest and profit. Furthermore, the post-Keynesian theory of classes is based on distribution (and not on production), and it is preoccupied with the problem of the rentier (an economic agent that supposedly hinders the proper functioning of the capitalist system). It identifies modern rentiers with financiers. Thus, it separates them and pits them against the other two fractions of the capitalist class; thus, ignoring their primary common interests and their complementary roles (despite their secondary antagonisms).

The MR School was the forerunner for the introduction of financialization in the Marxist tradition within which some remain in the Marxist analytical framework whereas others have a rather Marxisant flavor as they abandon its critical features.

The Marxist versions analyze financialization via the labor theory of value (LTV) and by focusing on the notion of fictitious-capital. Furthermore, they continue to consider financial profits as a redistribution of surplus-value. On the contrary, Marxisant versions argue that new forms of exploitation appear that are accompanied by new class structures and that the LTV cannot grasp these developments. Fine (2014) and the MR tradition offer prominent examples of the Marxist versions. Lapavitsas (2014) and Bryan, Martin and Rafferty (2008) represent Marxisant versions.

Fine considers financialization as the essence of neoliberalism. He defines financialization as the extensive and intensive accumulation of interest-bearing-capital (and fictitious-capital). The intensive accumulation is the proliferation of the mass of financial assets, which goes hand-in-hand with their growing distancing from production. The extensive accumulation is the encroaching of interest-bearing-capital into new fields of socio-economic life through novel hybrid forms (Fine 2014). Under such conditions, finance dominates capital accumulation via shadow banking. However, the financial system does not acquire autonomous channels of exploitation of labor. The novel forms of money-capital and institutional arrangements are policies that are used by capital to surpass its contradictions. Hence, Fine keeps the Marxist tradition that relates finance to the sphere of production and considers financial profit as part of the surplus-value. But, he does not coherently relate the emergence of financialization as a structural break and the 2008 global crisis to profitability.

The MR argues that monopoly capitalism has evolved to a new phase of monopoly-finance capitalism as the system discovered novel ways of reproducing itself. More specifically, debt and speculation became instrumental in engineering growth periods. This was facilitated by neoliberalism and its deregulation drive as it unleashed finance. In this new phase, underconsumption is hidden as increasing income inequalities are covered by the snowballing indebtedness of households. At the center of this new phase stands finance capital which is defined broader than Hilferding (as encompassing the whole financial system and not only banking). The simplified versions of MR’s FH (Foster 2008) have significant analytical and empirical deficiencies. First, they do not coherently explain what this new finance capital is, how it came into being, and how it can boost accumulation. Second, they rely heavily on Minsky’s Financial Instability Hypothesis, which divorces the financial system from real accumulation; an issue rightfully criticized by the Marxist tradition.

Guillen (2014) offers a more thoughtful version by arguing that as capitalism passes from different stages its three generic fractions (productive-, money-, and merchant-capital) change. In monopoly capitalism, their differences (and the differences between the types of profit they receive) are blurred. He maintains that Hilferding had (apart from his typical definition of finance capital) another more coherent definition that identifies it with the segment of capital that controls the issuance and circulation of fictitious-capital. In monopoly capitalism this finance capital is dominant but there are periods of financialization and periods of non-financialization. In modern capitalism, this has evolved to monopoly-finance-capital. This new hybrid is based on the extraction of the promoter’s profit. Finally, following Arrighi (1994), he defines financialization as periods of “maturing and decline of the hegemonic powers” (Guillen 2014, 458). His analysis shares the general criticisms concerning MR’s monopoly theory and Hilferding’s promoter’s profit. Moreover, his adherence to Arrighi’s definition of financialization periods weakens the significance of financialization. Nevertheless, all versions of the MR consider financial profits as a redistribution of surplus-value and do not propose a separate mechanism of exploitation.

The Marxist FH versions make some interesting points despite having minor weaknesses. However, they are marginal within the FH tradition as heterodox and mainstream approaches predominate.

Lapavitsas’s financialization theory is closer to post-Keynesianism. He maintains that shadow banking makes traditional banking redundant. Consequently, the financial system becomes totally stock-exchange-based. Lapavitsas (2014, 110) conflates interest-bearing-capital with loan-money-capital by downgrading the latter to a more concrete category and, hence, appropriate for analyzing financialization (as opposed to the abstractness of interest-bearing-capital). This is a sleight of hand because for Marx loan-money-capital is the general abstract concept out of which interest-bearing-capital and money-dealing-capital arise. Via this conflation, Lapavitsas, ultimately, foregoes the crucial distinction between money-as-money and money-as-capital. He rejects the concept of fictitious-capital as obscure (“a widow’s cruse”) and declares that new financial tools and processes are almost unrelated to the sphere of production and must be analyzed independently. Thus, the LTV and its monetary theory are effectively abandoned. He proposes the vague notion of finance as capitalism’s new core. To evade the critique of suggesting two separate capitalist classes he contends that finance subsumes and restructures the productive-capital. So, there is no meaningful distinction between them, and productive- and money-capital (taking merchant-capital along) have become unified. But, curiously enough, finance has a serious difference from the other two. It acquired a separate channel of direct exploitation of workers through the provision of usurious loans: “These practices are reminiscent of the age-old tradition of usury, but they are now performed by the formal financial system” (Lapavitsas 2009, 111). He terms this new source of financial profit financial expropriation. This autonomous source enables financial institutions to increase their profits independently of surplus-value and possibly to exploit us all (Lapavitsas 2014), alluding to the financial expropriation of other social strata apart from labor. While he rejects Hilferding’s promoter’s profit as problematic, he essentially inflates it. In his logic, finance exploits its oligopolistic position and amasses extra revenues (from fees, etc.) not only from other capitalists but also from every other social stratum that falls into its hands. This is indeed akin to Hilferding’s promoter’s profit but with a major difference. Although the promoter’s profit is a part of surplus-value for Hilferding, for Lapavitsas profits from financial expropriation are not. For him, this new structure constitutes a new social order, which is essentially the alias for a new stage. Furthermore, for Lapavitsas there is no general Marxist theory of crisis but each crisis is historically specific. Of course, there are crises in capitalism not directly related to falling profitability, and Marx and the Marxist tradition recognize it. But, at the level of general (abstract) theory, all different Marxist approaches (the falling rate of profit, underconsumption, disproportionality, etc.) define a basic mechanism generating crises in capitalism and they relate it to profitability. Lapavitsas departs from this. Characteristically, he considers the 2008 crisis as the hallmark of the new financialization epoch as unrelated to profitability (Lapavitsas and Kouvelakis 2012).

Bryan, Martin and Rafferty (2008) contend that since the early 1980s finance became commodified through several financial innovations (securitization, derivatives, etc.). Although evading branding this as a new capitalist stage (Bryan 2010), they infer so. For them, increased leverage and derivatives and workers’ financial exploitation through usury alter fundamentally capitalism’s functions and class structure. They claim that labor became a form of capital because the reproduction of labor is now a source of surplus-value transfer (through interest payments and the financialization of daily life). Thus, capitalist exploitation is not only unpaid labor-time but also usurious interest payments. Additionally, if labor has become a form of capital this entails directly that a new class structure different from typical capitalism has emerged. Among the other problems in their analysis, the most prominent is the flawed idea that derivatives obtain money functions.

The Marxisant versions of the FH essentially adopt the post-Keynesian endogenous money theory. They discard (or deform beyond recognition) the crucial Marxian concept of fictitious-capital and ultimately concur with the mainstreamers and the post-Keynesians that the unproductive-capital dominates productive-capital, and that the former acquires autonomous (from surplus-value) sources of profit. Consequently, they converge to a great extent with the Keynesian theory of classes and consider industrialists and financiers as separate classes. For Keynesian analysis, this is not a problem as it posits that different factors affect savings and investment. However, Marxism conceives money and productive-capital as forms of total capital that both take part in the formation of the general rate of profit (which among others is a process unifying the bourgeoisie against the proletariat). Therefore, since interest is part of surplus-value and financial profits depend upon the general rate of profit, Marxism does not elevate the distinctiveness of money-capital and productive-capital to the point of being separate classes. Finally, the Marxisant FH currents have a problematic crisis theory. Instead of a general theory of capitalist crisis, they opt for a conjunctural one. Each historical era and each particular crisis have their own specificities. But fundamentally, as Tomé (2011) demonstrates, the FH eventually ascribes to a Keynesian possibility theory of the crisis which has well-known shortcomings.

In conclusion, the FH variants fail to offer a realistic account of the rise of fictitious-capital activities during the recent period of weak profitability and increased over-accumulation of capital. Mavroudeas and Papadatos (2018) have shown that the classical Marxist perspective—based on the distinction between interest-bearing-capital and money-dealing-capital and by applying the notion of fictitious-capital—explains satisfactorily periods of increased financial profitability and also the creation of novel financial instruments (derivatives, repos, etc.) for these developments. Moreover, it does so by realistically keeping the primacy of the production sphere over circulation and also the notion that interest is part of surplus-value extraction.

The Empirical Myths of Financialization

Whatever theoretical perspective is taken, financialization must be accompanied by a series of empirical developments. For example, Fine (2019, 4) suggests that “just a few hundred multinational corporations . . . run the world economy” and “of these, two-thirds are financial companies.” Further, he associates financialization with “the extraordinary rise of finance” and argues that “the ratio of financial assets to economic activity increased threefold over the past thirty years.” He asks “why, on average, should it take three times as much finance to produce something as previously?” According to Sawyer (2016), financialization involves the growth of the financial sector which has become too large. Ashman and Fine (2013) suggest that finance expands at the expense of real investment. Financialization, therefore, is an important cause of deindustrialization (Palley 2013; Davis 2018). It is often claimed that financialization is largely due to financial liberalization (Krippner 2011; Soener 2020). And while financialization develops at different paces and forms it has a global reach and therefore is a global phenomenon (Bonizzi 2014; Sawyer 2016). These are empirically testable claims that will be reviewed and shown to be largely myths.

It should be noted at the outset that we do not aim to assess all the empirical claims of the financialization thesis which are numerous. The big rise in financial corporations’ profit as a percentage of the profit of all corporations in the US, for example, could be considered as one measure of the growing role of the financial sector. While such measures are relevant to the scope of our article, we limit our focus to the ones mentioned above. Hence, our empirical work characterizes as myths the specific empirical beliefs that are scrutinized in this article.

Myth 1. Two-Thirds of the Few Hundred Largest Multinational Companies Are Financial

At first glance, the empirical evidence seems to support this claim. Forbes’ (2018) data suggests that eight out of ten (80%) largest multinational companies are financial (Figure 1A). A closer inspection of the data, however, unfolds a rather different picture.

First, as the number of the largest companies increases, the share of the financial companies declines rapidly. The figure declines to 44% for the largest 50 multinational companies, 39% for the largest 100 multinational companies, 31% for the largest 500 multinational companies, and 17% for the largest 1000 multinational companies. The suggestion that two-thirds of the few hundred multinational companies are financial, therefore, is not supported by the evidence. It is also interesting to note that five out of the eight largest financial multinational companies are Chinese.

Second, Forbes uses four different measures to create its ranking, which are assets, sales, profits and market value. The ranking of the financial multinational companies is heavily influenced by the assets component, which needs careful elaboration. Figure 1B shows the ranking of multinational companies in terms of assets and indicates a more favorable ranking for financial multinational companies. This time, nine out of the ten largest multinational companies are financial. The figure increases to 92% for the largest 50 multinational companies and then declines to 87% for the largest 100 multinational companies, 33% for the largest 500 multinational companies, and 17% for the largest 1000 multinational companies.

The ranking of multinational companies in terms of assets, however, is problematic because the largest proportion of banking assets are loans and securities held. In the US for example, loans (52.6%) and securities (20.7%) held accounted for 73.3% of the banking assets in 2014 (Perez 2015). As opposed to these assets, banks also have liabilities (i.e., deposits) that need to be considered. The assets component of the Forbes figures, therefore, exaggerates the real size of the financial multinational companies. This can be seen in Figure 2, where 39 financial and 61 non-financial multinational companies in the top 100 multinational companies are compared. Assets and market value of companies are normally expected to be closely linked. This is true for non-financial multinational companies, where assets are slightly higher than market value. For financial multinational companies, however, assets are 11.4 times higher than their market value. The ranking of financial multinational companies in terms of assets is problematic and the inclusion of assets in the final Forbes ranking also exaggerates the significance of financial multinational companies.

Comparing 39 Financial (F) and 61 Non-financial (NF) Multinational Companies in Terms of Sales, Profits, Assets and Market Value (Billion US Dollars)

Notes: Calculated by using averages.

Source: Forbes (2018).

The ranking of multinational companies in terms of sales (Figure 1C), profits (Figure 1D) and market value (Figure 1E) provides a much modest share for the financial multinational companies, particularly when Chinese financial multinational companies are excluded. Figures are as low as 10% and they barely exceed 20%. They are nowhere near two-thirds of the multinational companies.

The US and the UK come to mind first when considering financialization. Indeed, among the largest 100 financial multinational companies, the US has 40 and the UK has eight companies. There are some surprising results, however, when countries and regions are ranked by the number of large financial multinational companies. The ranking of the countries and regions according to the number of financial companies among the top ten companies will be considered first (Figure 3). Looking at the 28 countries and regions (for which the data is available) reveals that the most financialized countries and regions are neither the US nor the UK, but China, 1 Canada, and the United Arab Emirates (Figure 3A). According to this ranking, the UK leaves 22 and the US leaves only ten countries and regions behind.

Ranking of Countries and Regions in Terms of Financial Multinational Companies in the Ten Largest Multinational Companies

Notes: Here China refers to China’s mainland, Taiwan is China’s province, and Hong Kong is China’s Special Administrative Region (SAR).

Source: Forbes (2018).

The ranking of countries and regions changes considerably when the components of the Forbes measure are considered. The US is ranked first in terms of assets but ranked ninth in terms of profits, 13th in terms of market value, and 23rd in terms of sales. The UK is ranked fourth in terms of assets but ranked eighth in terms of sales, 14th in terms of market value, and 20th in terms of profits. Surprisingly, these countries and regions fall behind in the rankings.

Considering 11 countries and regions that have data for the largest 40 multinational companies reveals that the US is ranked second behind China in terms of assets but ranked eighth in terms of sales, profits and market value (Figure 4). The UK is ranked fourth in terms of market value, fifth in terms of assets, sixth in terms of sales and profits. Remarkably, regions and countries such as China’s mainland, China’s Taiwan, and South Korea, which are associated with industrialization are ahead of the US and the UK in this ranking. Even India and Hong Kong SAR of China appear to have more financial companies than the US and the UK.

Ranking of Countries and Regions in Terms of Financial Multinational Companies in the 40 Largest Multinational Companies

Notes: Here China refers to China’s mainland, Taiwan is China’s province, and Hong Kong is China’s Special Administrative Region (SAR).

Source: Forbes (2018).

Thus, the suggestion that two-thirds of a few hundred multinational companies are financial is incorrect, and the leading countries are not the US and the UK, but China, which is not associated with financialization.

Myth 2. The Ratio of Financial Assets to Economic Activity Increased Threefold over the Past 30 Years

This section analyzes the change in the share of the financial sector (finance and insurance) value added in total national income in 41 countries to assess the claims that the financial sector has expanded significantly during the last 30 years. Data availability (beginning and end of the data) varies by country and ranges from 13 years to 48 years, but our analysis is limited to the 1989–2018 period (past 30 years). The selection of this period is both determined by concerns over optimizing our data as well as Fine’s (2019) focus on this period. It should be noted, however, that the big rise in the share of the financial sector in many countries may have occurred from around 1980 to 2000. Utilizing the trend from 1989 to 2018, therefore, may miss a portion of the period of expansion.

Figure 5 shows that the share of financial sector value added in 2015 was above 10% for only two countries: Luxembourg and South Africa. While the financial sector share in 19 countries is between 5% and 10%, it is below 5% in the other 20 countries. The US (7th) and the UK (11th) are ranked relatively high but South Africa and China are ranked higher than the US and Brazil is ranked higher than the UK. Portugal (5.3%), Greece (4.5%) and Spain (4.0%), which were among the countries most affected by the 2008 crisis, are far behind on the list. The relative size of the financial sector does not seem unusual except in a few countries.

Ranking of Countries according to the Share of the Financial Sector in Total Value Added (% in 2015)

Source: Author’s calculation based on OECD (2019).

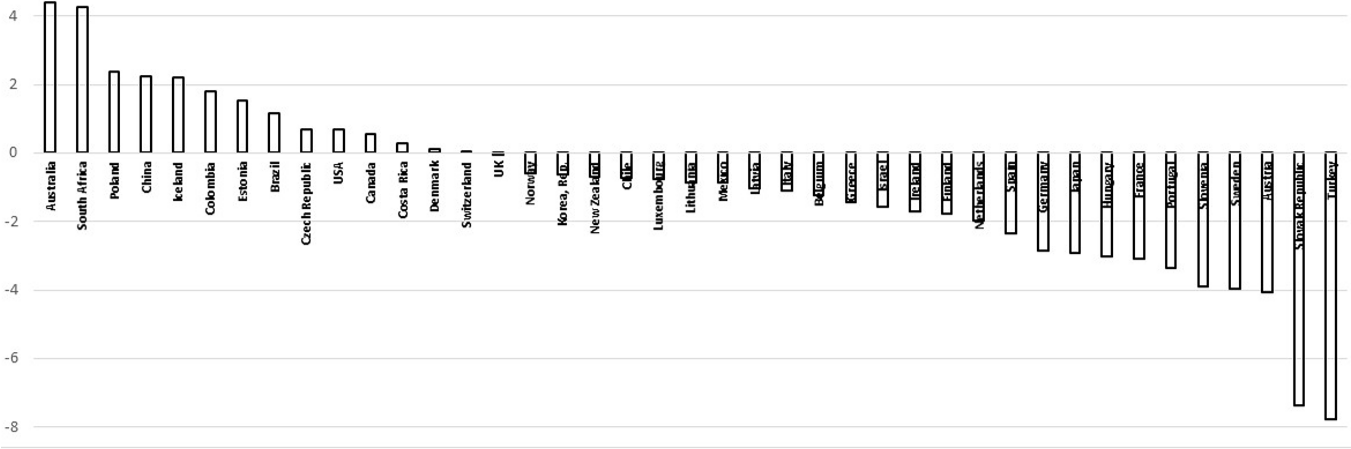

The findings are more striking when considering the same countries in terms of the change in the share of the financial sector in national income. Figure 6 shows that the financial sector share increased in 20 countries and decreased in 21 countries (indicating de-financialization) which refutes the claim that financialization is a global phenomenon. The fastest financializing countries are South Africa (4.50%), China (4.06%), Australia (3.81%) and Luxembourg (3.09%). Most countries experienced modest increases. The US is ranked 11th (by a 1.19% increase) and the UK is ranked 13th (by a 0.83% increase) in the list. Only five countries experienced an increase between 2% to 4.5% and 15 countries less than 2%. None of these figures implies a significant rise in the share of the financial sector. Portugal, Greece and Spain are among the 21 countries that experienced de-financialization.

Change in the Share of the Financial Sector in GDP % (Estimation for 30 Years)

Notes: Since data availability varies by country, 30 years of data have been estimated by using the available data.

Source: Author’s calculation based on OECD (2019).

The idea that the rate of economic activities of the financial sector has tripled in the past 30 years, therefore, is another myth. The OECD (2019) database shows that although the share of the financial sector in national income increased (due to the financial bubble) in many countries until the 2008 crisis, this situation was not permanent and decreased after the crisis. Indeed, the share of the financial sector in national income increased in 26 (65%) of 40 countries before the financial crisis (between 2000 and 2007), it declined in 24 countries (60.0%) after the crisis (between 2007 and 2018). Between 2000 and 2018 it increased in 19 countries (47.5%) and declined in 21 countries (52.5%).

Myth 3. Financialization Is an Important Reason for Deindustrialization

The conflict between financial and productive-capital is at the heart of the financialization debate. Very often the expansion of the financial sector is held responsible for the decline in the productive (manufacturing) sector which is one of the main themes of the FH.

Financialization is associated not only with the increase in the number and power of financial companies but also with the increasing penetration of non-financial companies into financial markets (Davis and Kim 2015). In this view, non-financial companies increasingly substitute real investments with financial investments which contribute to rapid deindustrialization, slow growth, lower profits and economic crises (Krippner 2005; Baud and Durand 2012; Palley 2013; van der Zwan 2014; Dünhaupt 2017; Davis 2018).

Rabinovich (2019) tested this thesis for US companies and showed that only 2.5% of the total revenues of non-financial companies are financial. It has also been shown that the share of financial income in these non-financial companies, which started to increase in the 1990s, has decreased since 2005. By focusing on non-financial companies in the largest 37 countries from 1991 to 2017, Soener (2020) raises doubts about the overall validity of corporate financialization. He finds no evidence of real investment being substituted with financial investment and suggests that the shares of financial assets and income have fallen over time.

Alternatively, the slowdown in investment rates has been argued to be at the heart of financialization. In this view, the decline in profitability stimulated non-financial companies to focus on financial activity instead (Brenner 2003; Krippner 2005). In a cross-country analysis of 17 OECD countries for the 1997–2007 period, however, Karwowski, Shabani and Stockhammer (2017) found no indication that investment slowdown precedes financialization.

The empirical evidence, therefore, is at best inconclusive since there are conflicting findings in the literature. The issue is made even more complicated by the fact that the financialization of non-financial firms is often concealed with the help of accounting techniques (Prechel 2021).

There is little doubt that the share of the manufacturing sector in total value added declined in most countries and the share of financial services increased in many. However, such a simple observation does not lend credibility to the idea that financialization is responsible for deindustrialization, as significant increases are also observed in non-financial service sectors. The purpose of this part, therefore, is to examine the extent to which the decline in the manufacturing sector can be associated with an increase in the financial sector.

It should be noted at the outset that the following analysis will investigate the link between the share of the financial sector and the share of the manufacturing sector. An increase in the share of one sector must necessarily be associated with a decline in the share of other sectors. Such a simple association between sector shares establishes no theoretical causality and should be considered indicative only. However, if an increase in the share of the financial sector is not associated with a decline in the share of the manufacturing sector, there is a reason not to link financialization with deindustrialization.

Figure 7 shows that the share of financial services in total services declined in 27 (65.9%) countries and increased in 14 (34.1%) countries over the past 30 years (1989–2018). This implies that service sectors other than financial services may have contributed more to the decline in the share of the manufacturing sector in these countries.

Change in the Share of Finance in Services % (Estimation for 30 Years)

Source: Author’s calculation based on OECD (2019).

This observation is important because some authors have argued that financialization shifted the gravity of economic activity not only from production but also from much of the growing service sector to finance (Foster 2007).

Although the above observation is meaningful, the data allow us to examine the contribution of the financial sector to the declining share of manufacturing, even if indirectly. For example, if a 10% decline in the share of the manufacturing sector in GDP is associated with a 10% increase in the share of the financial sector in a certain period (while there is no change in the share of other sectors), the increase in the financial sector can be said to be fully responsible for the decrease in the share of the manufacturing. If the 10% decline in the share of the manufacturing sector is associated with a 2% increase in the share of the financial sector and an 8% increase in other sectors, however, only 20% of the decrease in the share of the manufacturing industry is due to the expansion in the financial sector and 80% is due to the expansion in other sectors.

Of course, in any economy, there will be sectors with an increasing (decreasing) share besides the financial (manufacturing) sector. Therefore, it would be useful to look at the share of the increase (decrease) in the financial (manufacturing) sector among other increasing (decreasing) sectors. To establish a meaningful link between financialization and deindustrialization, a significant increase (decrease) in the share of the financial (manufacturing) sector must be associated with a significant decrease (increase) in the share of the manufacturing (financial) sector.

Table 1 shows the percentage share of the proportional increase in the finance (manufacturing) sector among other rising (falling) sectors in 35 countries between 2000–2007 and 1995–2018. An example will help the reader understand the table. In Iceland, for example, the total share of five sectors in national income decreased and the total share of six sectors increased by 12.2% between 2000 and 2007 (Figure 8A). Two observations can be made here. First, the finance sector has been the sector whose share has increased the most (by 7.2%) among the six sectors and this is shown as 1/6 in parentheses in Table 1. And the manufacturing sector has been the sector whose share has decreased the most (by 4.3%) among the five sectors (1/5). Second, the share of the finance sector in all sectors whose share has increased is 59.4% (7.24/12.2 = 0.594) and the share of the manufacturing sector in all sectors whose share has decreased is 34.9% (4.25/12.2 = 0.349). It can be said, therefore, that the expansion in the financial sector is the most important determinant of the decline in the manufacturing sector in this country.

The Percentage Share of the Proportional Change in the Finance and Manufacturing Sectors among Other Sectors in 35 Countries

Source: Author’s calculation based on OECD (2019).

The Proportional Change in the Sectoral Share for Selected Countries

Notes: The sectors are agriculture, forestry, fishing (agriculture); manufacturing; construction; wholesale, retail trade, repairs, transport; accommodation, food services (wholesale); information, communication (Information); finance and insurance (finance); real estate (RE); professional, scientific, support services (professional); public administration, defense, education, health, social work (public); other services activities (other serv.); mining, water, gas, transport (MWGT).

Source: Author’s calculation based on OECD (2019).

The numbers in Table 1, therefore, are large if the expansion (decline) of the finance (manufacturing) sector is large. Multiplying these figures (0.594 and 0.349) also provides (0.207 or 20.7%) additional information. This figure will vary between 0 and 100% and indicate the importance of an increase in the financial sector on the decline in manufacturing. It will be large if the decline in manufacturing and the increase in finance are large. It will be 100%, for example, if the financial sector is the only sector that expands, and the manufacturing sector is the only sector that shrinks. In this case, the increase in the financial sector fully explains the decline in manufacturing. The figure will be small if the decline in manufacturing and/or increase in the finance sector is small. It will be zero if the financial sector declines or the manufacturing sector increases.

Under three scenarios the financial sector will not be responsible for the decline in manufacturing. First, the share of the financial sector may be small among sectors whose share in national income is increasing. In Latvia, for example, the share of the manufacturing sector decreased by 7.95% between 1995 and 2018 and the share of the financial sector increased only by 0.10% (Figure 7B). While the manufacturing sector declined the most among the declining four sectors (1/4) and was responsible for 46.8% of the total decline in these four sectors, the financial sector increased the least among the increasing seven sectors (7/7) and was responsible for 0.6% of the total increase in these seven sectors. Multiplying these figures produces 0.3%, indicating that the expansion in the financial sector is the least important determinant of the deindustrialization observed in this country. Real estate, science, information, construction, wholesale and other services contributed a lot more than the financial sector to deindustrialization.

Second, the share of the financial sector can decrease. In the Slovak Republic, for example, there is a decrease in both the manufacturing industry’s share (3.4%) and the financial sector’s share (3.2%) between 1995 and 2018 (Figure 7C). While the manufacturing sector declined the most among the declining five sectors (1/5) and is responsible for 26.9% of the total decline in these five sectors, the financial sector is not responsible for deindustrialization in this country.

Third, the share of the manufacturing industry may be increasing. Between 1995 and 2018, the share of the manufacturing industry in national income increased in countries such as Ireland, South Korea, the Czech Republic, Hungary and Lithuania. In Ireland, not only the share of the manufacturing sector expanded but also the finance sector shrunk (Figure 7D).

Under these three scenarios, it would not be meaningful to talk about deindustrialization or to keep the financial sector responsible for it.

It is useful to examine the data in two separate periods, 2000–2007 and 1995–2018. In most of these countries, there was an extraordinary increase in the share of the financial sector due to the bubble economies that occurred during the 2000–2007 period. Therefore, it can be expected that the effect of the expansion in the financial sector on the manufacturing industry (and other sectors) will be stronger in the 2000–2007 period. Examining the same relationship between 1995 and 2018 will show how the relationship between finance and the manufacturing industry has changed over a longer period. The cells where zero is entered in the table show either a decrease in the share of the financial sector or an increase in the share of the manufacturing industry, in which case there is no evidence to support the financialization thesis.

A detailed examination of the table provides some interesting findings. First, there is no meaningful relationship between “financialization” and deindustrialization (zero values in the table) in 16 countries (45.7%) in the period 2000–2007 and for 20 countries (57.1%) in the period 1995–2018. There is a meaningful link in only ten countries (28.6%) between the financial and manufacturing sectors in both periods. In 11 countries (31.4%) there is no meaningful link in both periods and in 14 countries (40%) there is a meaningful link in only one period. Therefore, only in ten countries, the financialization thesis can somehow be supported.

A closer inspection of these figures is needed to assess how important is the financial sector expansion for the decline in manufacturing in these countries. In only 11 countries the figures in Table 1 for the financial sector exceeded 20% and only in four countries exceeded 30% in the 2000–2007 period. In the 1995–2018 period, only one country exceeded 20% and no country exceeded 30%.

In the 2000–2007 period, the “construction” sector was the fastest-growing sector in seven countries, science in six countries, finance and RE in five countries, public in four countries, MWGT in three countries; manufacture and wholesale in two countries, and information in one country. In the 1995–2018 period, the science sector was the fastest-growing sector in 19 countries, RE in seven countries; MWGT, public and wholesale in two countries; construction, information, and manufacture in one country. In no country was the finance sector the fastest-growing sector in the 1995–2018 period. In the 2000–2007 period, the financial sector was ranked first in five countries and was ranked second in four countries. In the 1995–2018 period, while there was no country in which the financial sector was ranked first and second, only in four countries it was ranked third. Also, the increases observed in the share of the financial sector in the 2000–2007 period were reversed in the 1995–2018 period and most countries experienced a rapid decline. For example, the figure went down from 59.4% to 14.7% in Iceland, from 57.3% to 20.8% in Luxembourg, and from 46.3% to 6.7% in the UK.

These findings suggest that sectors other than the financial sector may have played a more significant role in the decline of the manufacturing sector. The expansion in the financial sector may have contributed most to the decline in the manufacturing industry in the 2000–2007 period, which indicates that financialization is a cyclical development specific to this period. In the 1995–2018 period, the increase in the professional, public, and information services and real estate sectors came to the fore rather than the increase in the financial sector.

To support this discussion, Figure 9 shows the average change in the share of sectors for four periods in 35 countries. In the 2000–2007 period, the finance sector was the fastest-growing sector after the science and construction sectors (Figure 9B). As opposed to this, the share of both finance and construction sectors decreased in both the 1995–2000 (Figure 9A) and 2007–2018 (Figure 9C) periods. The decline in both sectors is remarkable in the 2007–2018 period. As a result, in the 1995–2018 (Figure 9D) period, the share of both sectors declined slightly. While the manufacturing and agriculture sectors declined significantly in all periods; science, RE, and information and public are the increasing sectors. The increase in science is particularly noteworthy.

Average Change in the Share of Sectors (%) for Four Periods

Source: Author’s calculation based on OECD (2019).

In conclusion, it is another myth that financialization played an important role in deindustrialization. Although a relative shrinkage was observed not only in the manufacturing industry but also in other sectors due to the expansion in the financial sector due to the bubble economies formed in 2000–2007, a normalization trend started with the collapse of the bubble.

Myth 4. Financialization Originated from Financial Liberalization

Another argument of the FH is that financialization is related to financial liberalization (Karwowski, Shabani, and Stockhammer 2017; Krippner 2011; Soener 2020). The fact that countries such as China and South Korea, which are not financially liberal and not identified with financialization, are at the forefront of financialization shows the importance of testing this thesis empirically.

The following simple regression analyses were used to test this thesis. The first regression examines the relationship between the share of the financial sector in national income and financial freedom for 2007 just before the crisis, while the second regression examines the same relationship in terms of changes between 1998–2007. The selection of the period for the second regression is determined by data availability. 2

Financial sector share = f (financial freedom)

Change in financial sector share = f (change in financial freedom)

In other words, the first regression aims to analyze the effect of financial liberalization level on the financialization level and the second one aims to analyze the effect of change in financial liberalization on the financialization level (see Table 2).

Statistical Test of the Relationship between Financialization and Financial Freedom

Notes: The 37 countries were used in the analysis. The data has been converted into a logarithmic form. Dummy variables for Iceland and Turkey were used in the second regression since these countries created normality problems.

Source: Financial sector share data from OECD (2019) and financial freedom data from Heritage Foundation (2020).

The regression results in Table 2 show no significant statistical relationship between financial liberalization and financialization level, neither in terms of level nor change. Therefore, the view that financial liberalization is the main cause of financialization is another myth, and the reasons for the expansion of the financial sector in a certain period should be investigated more carefully.

The Special Case of China

Before completing this section, China deserves special attention. The above analyses indicate that China has a very large financial sector and large financial multinational companies. This bears the question of why this should be the case for a country that is associated with industrialization rather than financialization.

While there is growing literature on whether financialization in China promotes or hinders its economic performance (Wang 2015; Wu et al. 2020), Fine (2019, 4) suggests that “the Chinese state continues to hold considerable control over the use of finance, and directs it to investment rather than speculation.” Allen et al. (2012) further suggest that (while growing) the Chinese stock market is relatively limited and the expansion of the financial sector has not slowed down the growth of the economy.

We consider China a case that does not conform to the financialization models. While shadow banking has increased substantially in China since the 1990s, this does not conform with the financialization theories and models for the following reasons.

First, the Chinese financial system remains a bank-centered system (contrary to the stock market-centered systems) and banks are at the center of shadow banking. Sun (2019) accurately characterizes this as the banks’ shadow system (banks’ money creation through accounting treatments that generate liabilities from assets) as differentiated from typical shadow banking (credit creation by non-bank financial intermediaries through money transfer). In typical shadow banking (as practiced in the West and envisioned in financialization theories) the main funding source is mutual funds, with underlying assets such as sub-prime loans and other illiquid financial claims (e.g., asset securitization, repos). By contrast, China’s shadow banking system depends on banks’ shadow, with credit-money created through the expansion of liabilities with loan-like assets. The most important category is wealth management products (WMPs). Most WMPs are created and sold by banks in corporations with trust companies, brokers and security firms (Dang et al. 2019).

Second, China’s banking system is subject to significant state regulations, which have been on the rise since the 2008 global crisis. This is reflected in a steady decrease in WMP issuance since 2017 (Dang et al. 2019). This goes against the financialization literature which maintains that a market-based financial system that is increasingly deregulated is the fundamental characteristic of financialization.

Third, the Chinese financial system remains geared toward financing production (Sun 2019). Although credit-money creation is geared toward ripping financial profits in the financialization literature, in China it operates along typical Marxian lines, that is, it aims to bolster the real economy.

Conclusions

This article argued that the FH fails to present a credible analysis of contemporary capitalism and it is marred by both analytical and empirical weaknesses.

In analytical terms, all FH variants (with the noteworthy exceptions of Fine’s and Gullen’s analyses) err in considering the financial system as an autonomous producer of economic wealth; not only independent from “real accumulation” but also surpassing productive-capital in wealth-creating capacity. Especially the FH variants that propose a novel financial direct exploitation mechanism equate unwarrantedly capitalism with the pre-capitalist forms of finance that have ceased to exist long ago; mechanism equates unwarrantedly capitalism with the pre-capitalist forms of finance that have ceased to exist long ago. Moreover, the FH tends to interpret short-run and conjunctural phenomena (such as the rise of finance during the onset of a crisis) as long-run structural changes. Thus, in methodological terms, the FH is truly a middle-range theory crawling behind conjunctural events and unable to produce a general theory.

These analytical deficiencies are coupled with seriously flawed empirical expectations. This study tested several crucial FH empirical suggestions and showed that they are largely just myths. First, the claim that most of the largest multinational companies are financial is rejected. Second, regarding the share of the financial sector in national income and its change over the last 30 years, China is ahead of the US and the UK in terms of both level and rate of increase. China, known for its rapid industrialization, is not a country associated with financialization.

Another important fact that fails to support the FH is that over the last 30 years the financial sector share in GDP declined by 51.2% (Figure 6) and the financial sector share in services declined by 65.9% (Figure 7) of the countries in our study. Third, there is no evidence that the expansion in the financial sector is a significant predictor of the decline in the manufacturing industry. Although the rapid expansion in the financial sector observed in some countries before the 2008 crisis suggests that the financial sector may have played an important role in deindustrialization, this situation seems to be cyclical when it comes to a wider time frame.

Finally, there is no significant statistical relationship between financial liberalization and financial expansion.